Apple has announced the launch of a new feature called “Apple Pay Later” in its digital wallet, allowing customers to pay for online purchases in installments. This latest move sees the tech giant join a growing number of companies embracing the buy now, pay later trend.

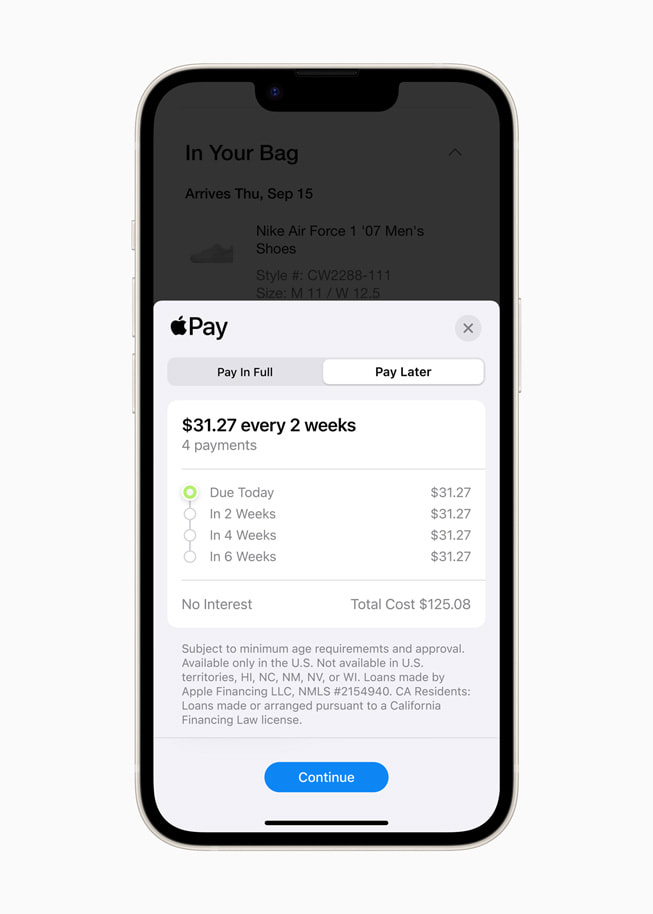

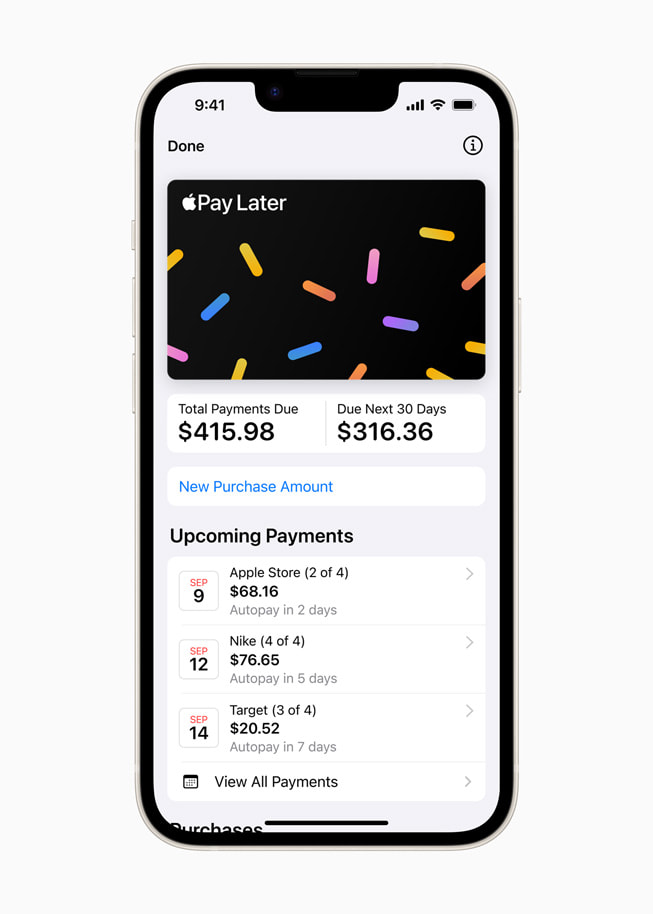

The new feature will allow users to split payments for purchases into four installments over six weeks, with the first installment due at the time of purchase. Additionally, Apple users will also be able to apply for a loan ranging from $50 to $1,000 within the Wallet app, with no interest or fees, to make online or in-app purchases.

While some have raised concerns that these types of services could cause shoppers to take on more debt, Apple says the new feature is “designed with users’ financial health in mind.” Jennifer Bailey, Apple’s vice president of Apple Pay and Apple Wallet, said, “There’s no one-size-fits-all approach when it comes to how people manage their finances. Many people are looking for flexible payment options, which is why we’re excited to provide our users with Apple Pay Later.”

The new feature will be rolled out to select users in the United States, with plans to offer it to all eligible customers over the next few months. Other popular services that offer the same payment option include Affirm, Klarna, and Afterpay.

The installment process makes it seem like customers are paying very little for the goods or services they’re acquiring, which has led to concerns that shoppers may take on more debt than they would if they had to pay for them in full each time.

However, Apple’s Pay Later option is enabled through the Mastercard Installments program, and Apple users will be able to track and manage upcoming loan payments in the Wallet app. The loan application can also be done in the app with no impact on credit, according to the company.

As more consumers turn to buy now and pay later services to stretch their budgets at a time of high inflation and broader economic uncertainty, companies are beginning to offer flexible payment options to meet this growing demand. By allowing customers to make purchases without having to pay the full amount upfront, buy now, pay later services are becoming increasingly popular, particularly among younger shoppers.

The move by Apple to launch Apple Pay Later is a strategic one, as it aims to compete with other payment services that offer similar payment options. According to a company release, the payment option is designed to offer users more financial flexibility and convenience, while still being mindful of their financial health.

Apple’s Pay Later feature is just the latest in a series of innovations aimed at making digital payments easier and more accessible for users. The company has been at the forefront of digital payments for several years, with the launch of Apple Pay in 2014 and Apple Card in 2019.

In addition to the new payment feature, Apple has also introduced several other updates to its Wallet app. Users can now add their driver’s license or state ID to the app, which will be available in select US states later this year. The app also supports home keys, allowing users to unlock their home with their iPhone or Apple Watch.

Overall, Apple’s entry into the buy now, pay later space with Apple Pay Later is likely to further disrupt the payments industry and provide consumers with more flexibility and convenience when it comes to managing their finances.